Farmer

Insights

2022

By Nelson Ferreira, Senior Partner

David Fiocco, Partner

Vasanth Ganesan, Partner

Maria Garcia de la Serrana Lozano, Associate Partner

Ana Luiza Mokodsi, Engagement Manager

Otto Gryschek, Director of Strategy and Operations

Global Farmer Insights

2022

By Nelson Ferreira, Senior Partner

David Fiocco, Partner

Vasanth Ganesan, Partner

Maria Garcia de la Serrana Lozano, Associate Partner

Ana Luiza Mokodsi, Engagement Manager

Otto Gryschek, Director of Strategy and Operations

McKinsey has surveyed 5,500+ farmers across the globe to better understand their mindsets and behaviors towards key topics shaping the future of agriculture

Key stats

Global Coverage

7

Geographies

~5,500

Farmers

1.5M+

Datapoints from global farmers

Cerrado

Centro-Sul

MATOPIBA

Sul

Geographies covered and farmers surveyed

5 themes shaping farming globally

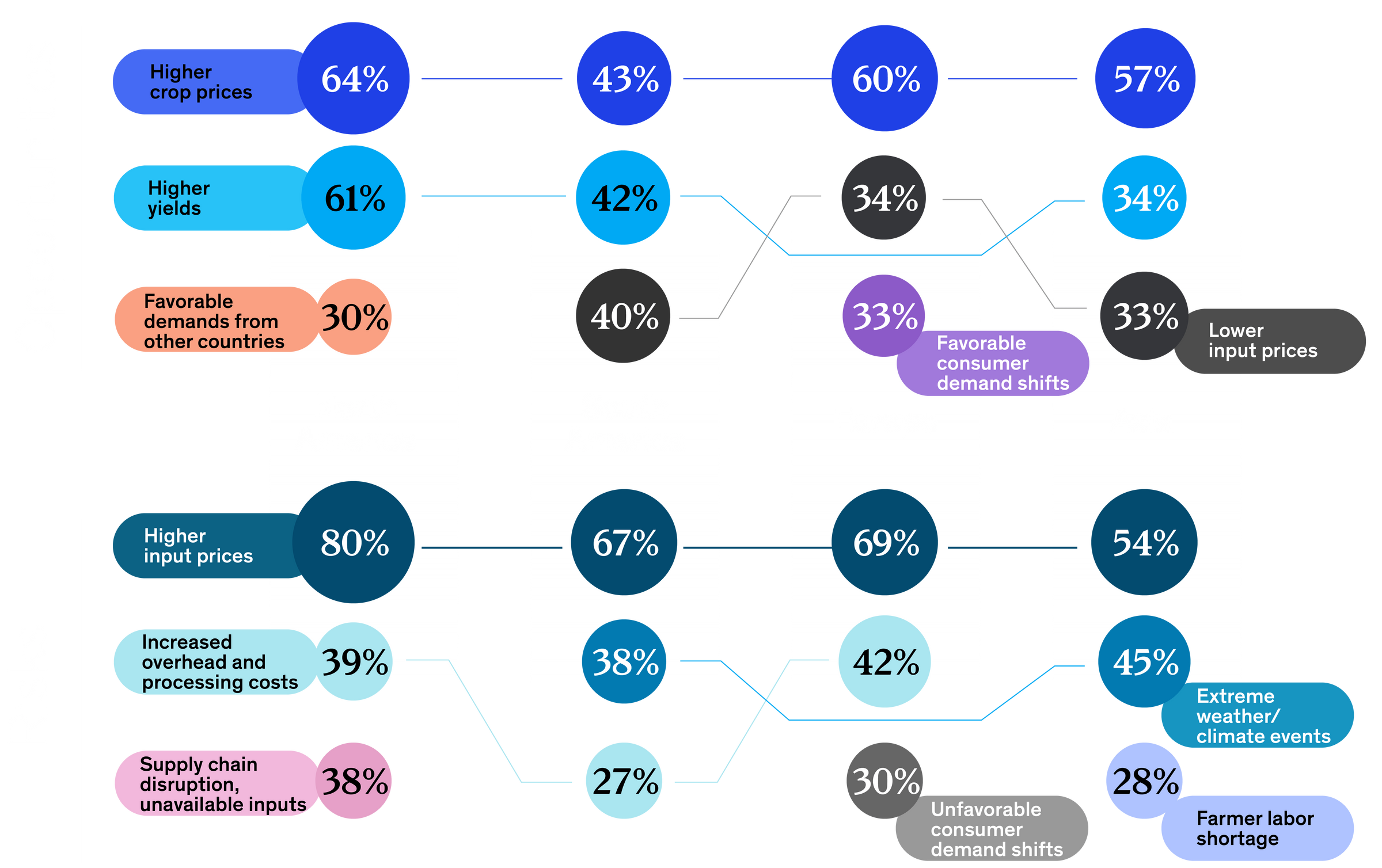

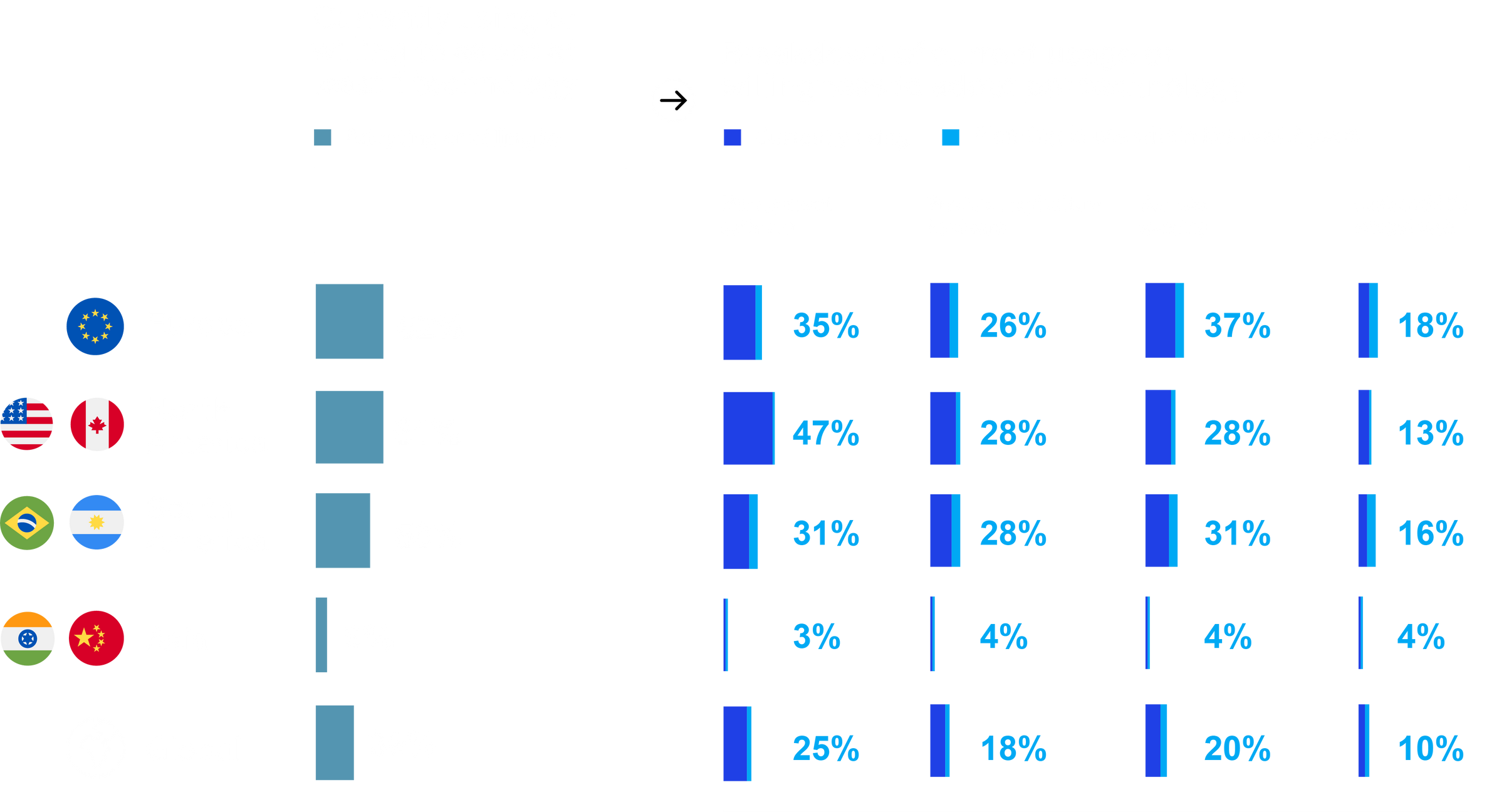

Farmers see high crop and input prices as the main tailwinds & headwinds respectively

Top 3 risks and opportunities to profits over the next 2 years

Q: What do you believe are the top 3 opportunities and risks to your profits over the next 2 years?; % of respondents (n=5,474)

Source: McKinsey’s Global Farmer Insights, May/2022

Farmers see high crop and input prices as main tailwinds & headwinds globally

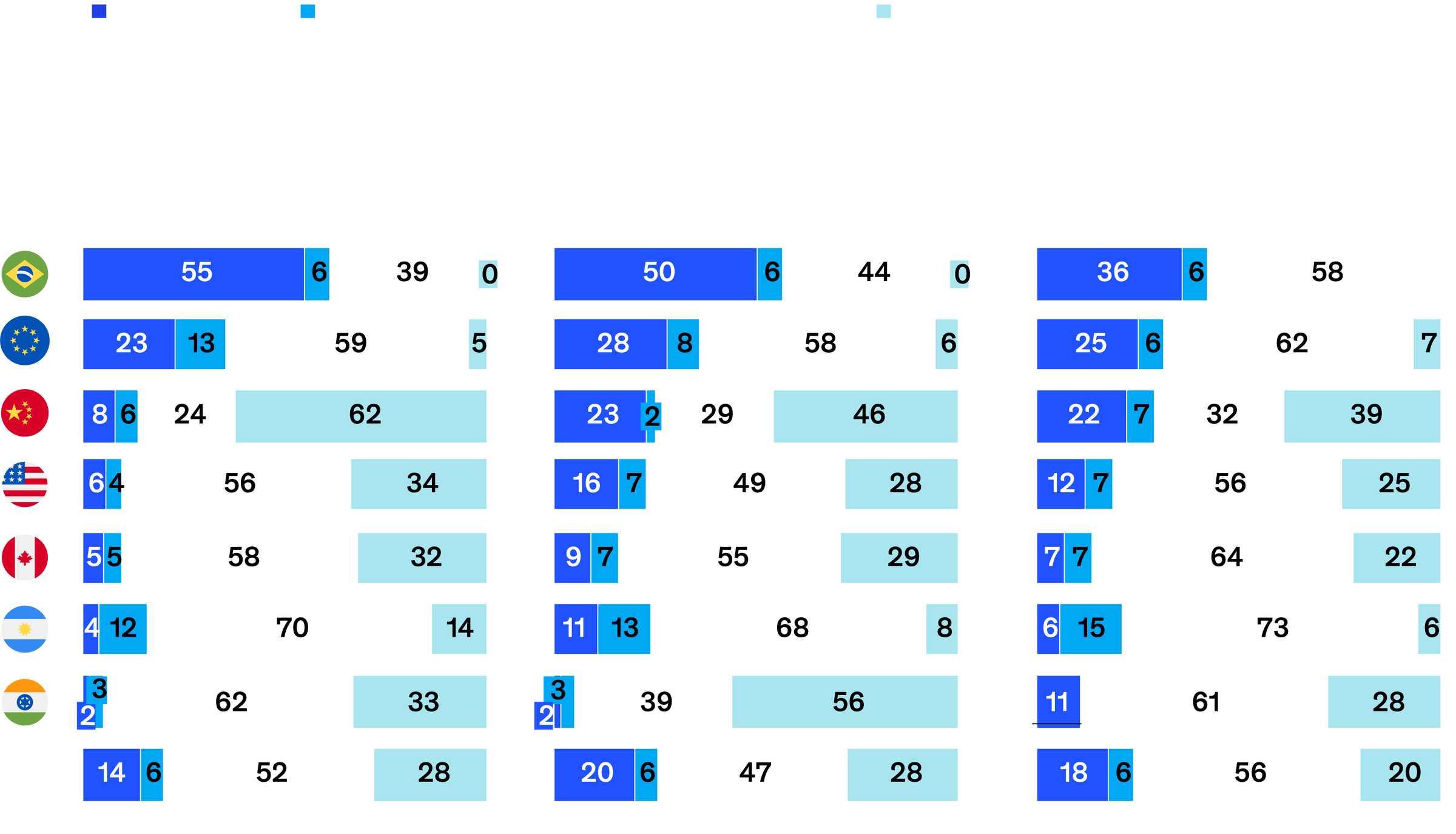

Actions to capture profit opportunity

Q: What actions do you anticipate taking to profit the most from those opportunities?;

% of respondents (n=5,474)

Source: McKinsey’s Global Farmer Insights, May/2022

Farmers anticipate using new products focused on yield productivity and crop protection to capture the high crop price opportunity

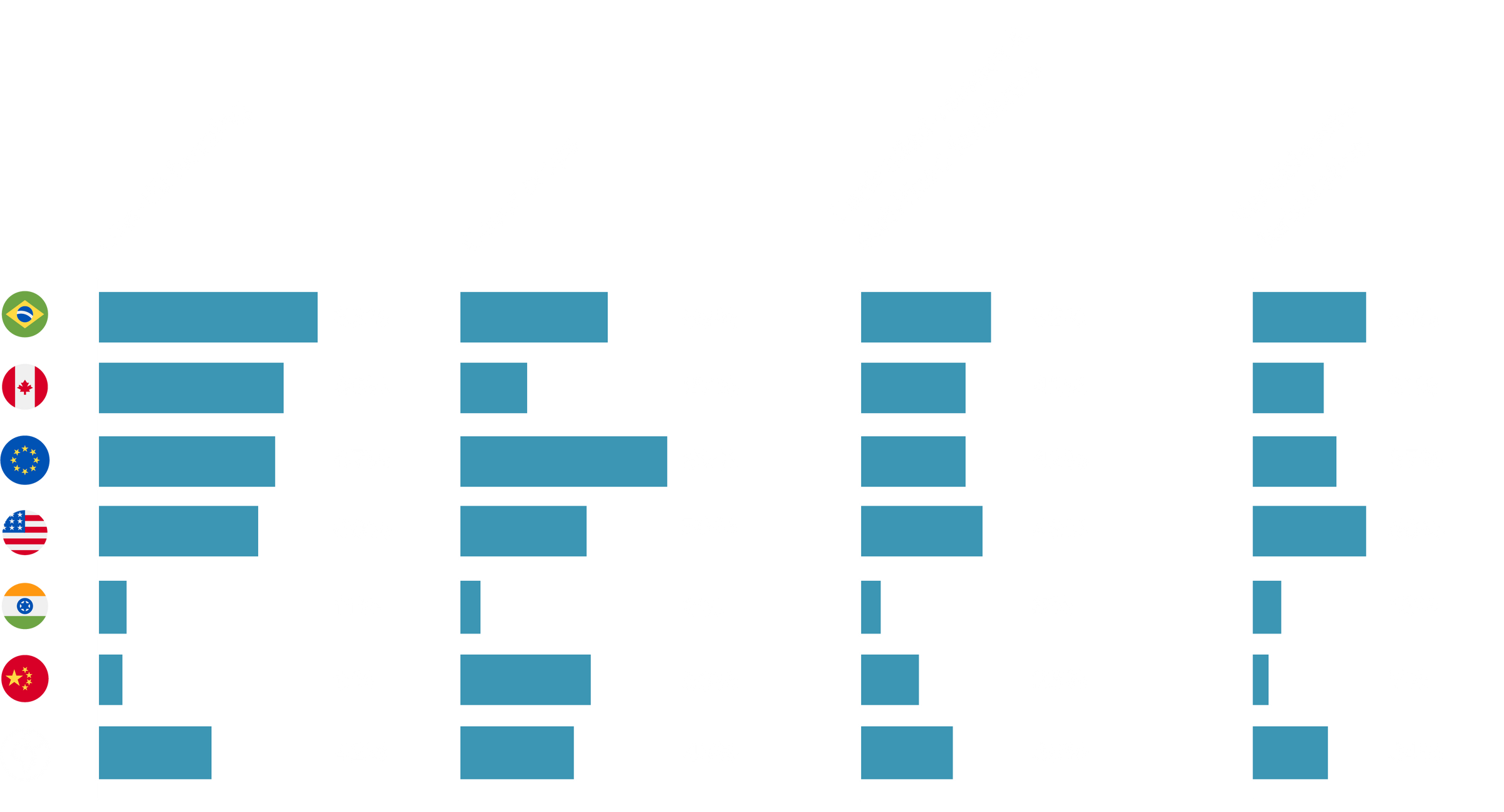

~50% of farmers already purchase at least one product digitally, South America leading the trend

Current usage of digital channels for agricultural purchases

% of farmers who use digital for the purchase of at least 1 product

Q: How do you currently make your agricultural purchases? % of farmers who use digital for the purchase of at least 1 product; (n=5,474)

Equipment and technology are expected to be the main products to be purchased through online channels in the next 2 years

Top products expected to be purchased online:

Equipment and technology are the main products expected to be purchased through online channels in the next 2 years

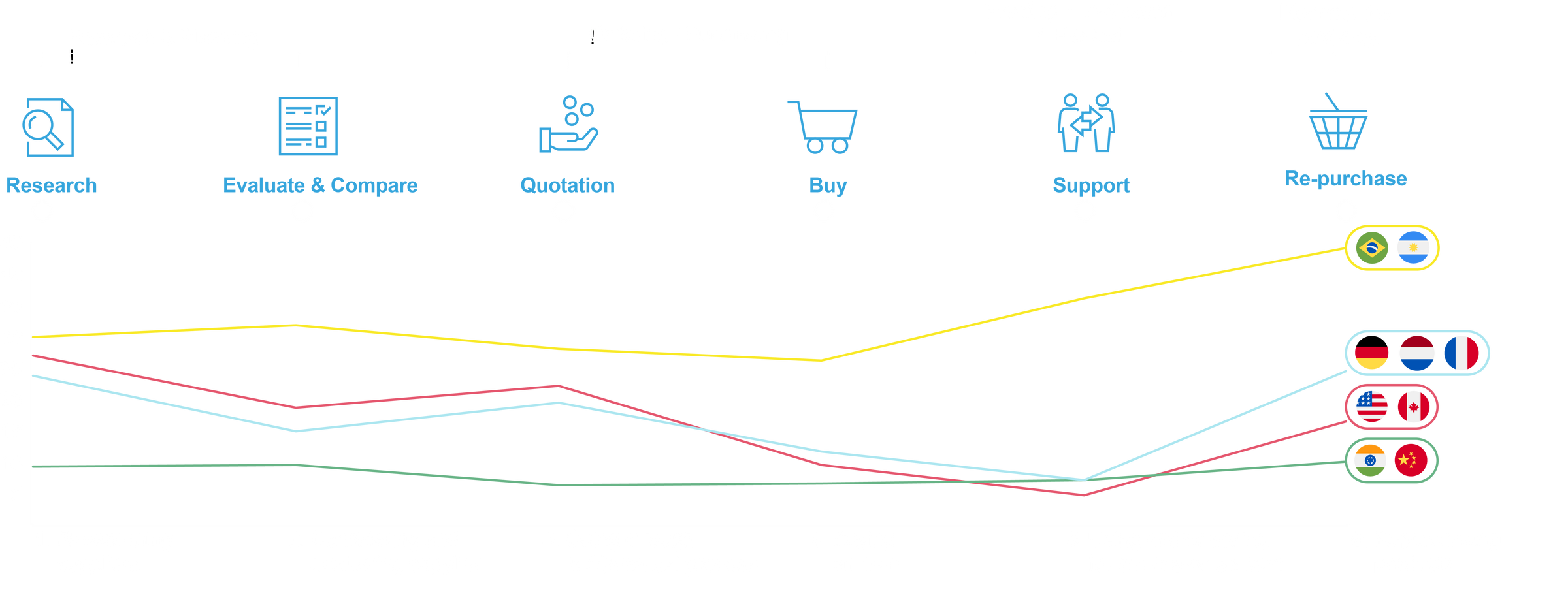

50% of farmers already blend digital with in-person/voice based interactions in their purchasing journey

Equipment and technology are expected to be the main products to be purchased through online channels in the next 2 years

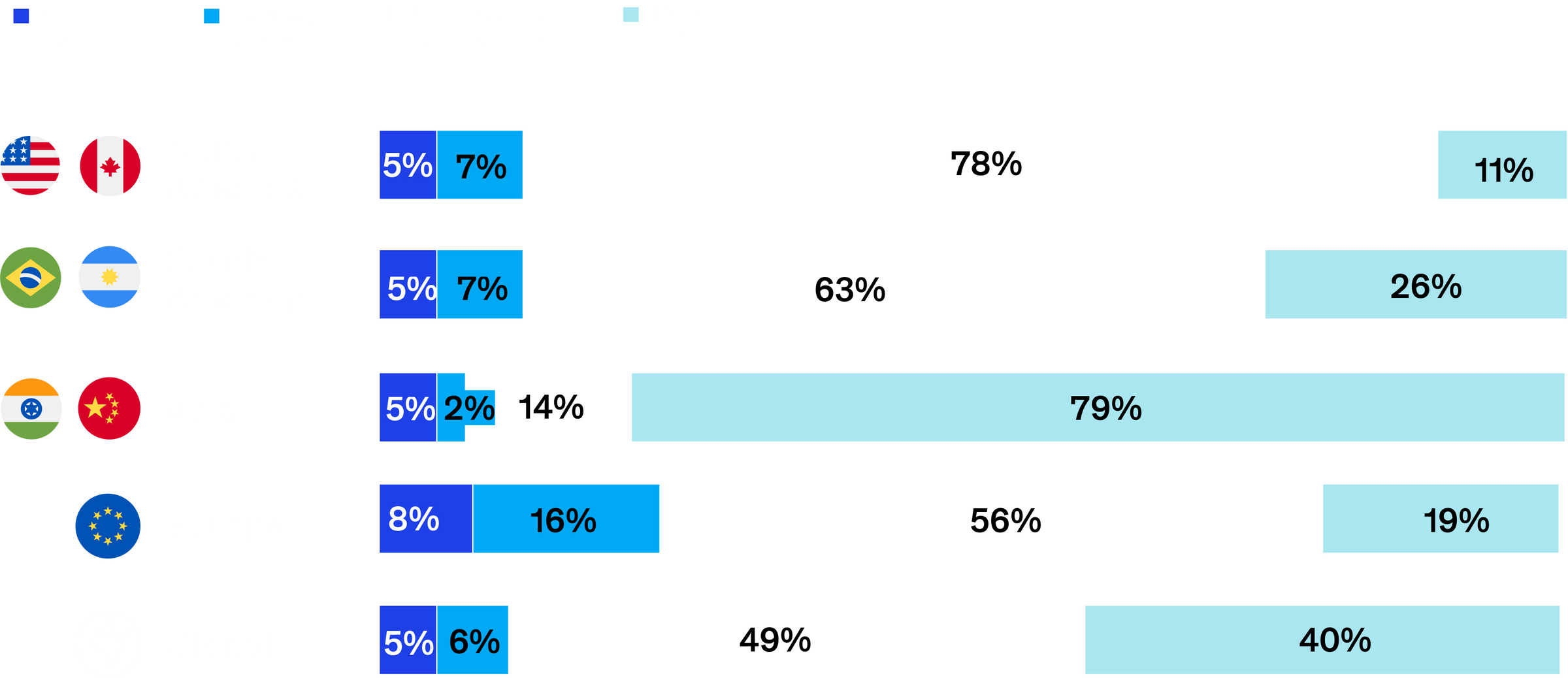

Preference for digital interactions

% of respondents who prefer digital interactions to in-person/voice interactions

Q: In an ideal world, how would you interact with companies for each type of activity listed below? (n=5,115)

Cash is the main payment method for agricultural purchases and digital payment is emerging as an important trend for farmers

Willingness to try digital payments

Q: What types of financial services would you like to try, given your needs?, Responses for Digital Payments; % of respondents; (n=5,474)

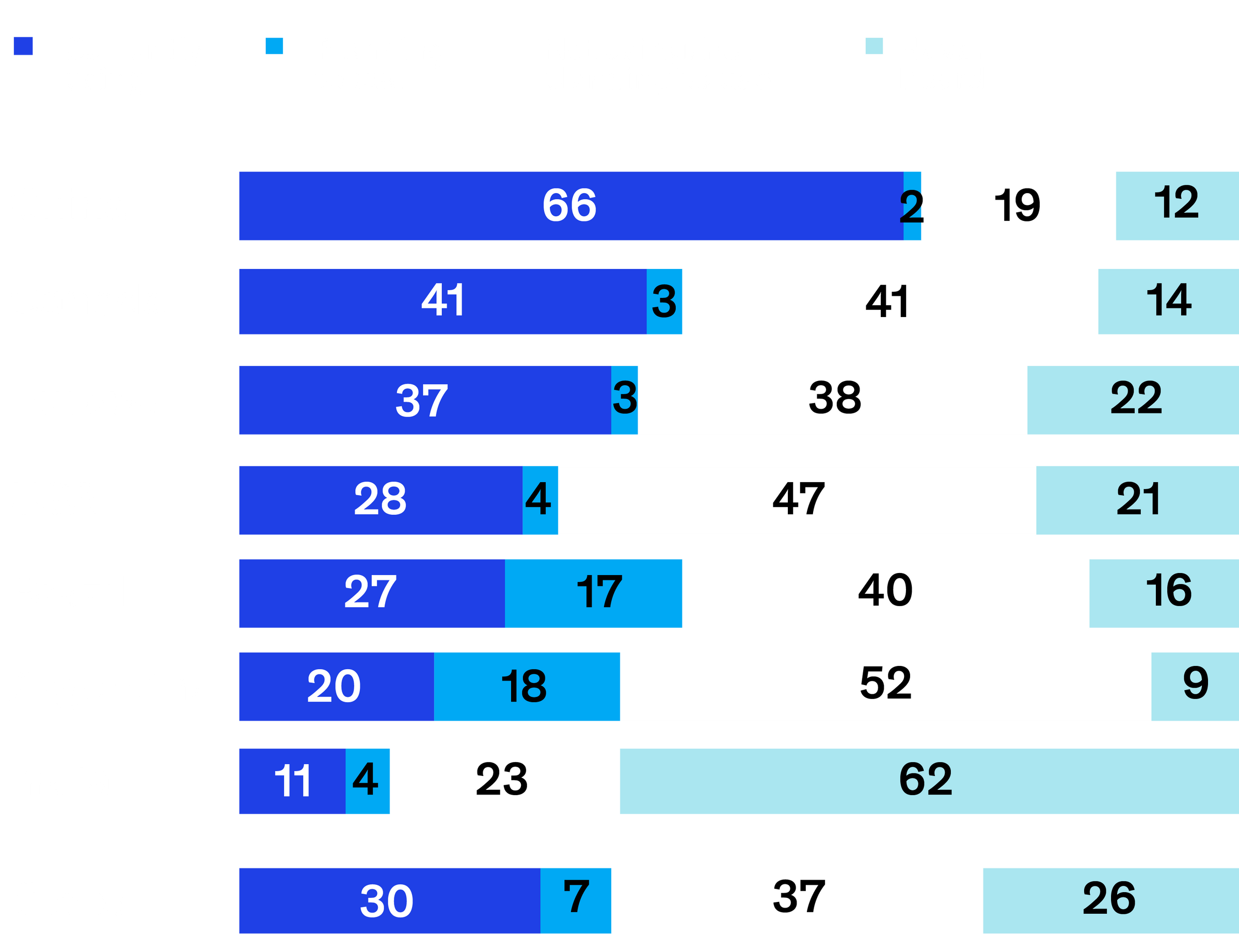

Western countries are leading ag tech adoption, with farm management software being the top technology

Farming technologies adoption and willingness to adopt

% respondents currently adopting or willing to adopt over the next 2 years

Q: What is your level of adoption regarding the following trends?; % respondents currently adopting or willing to adopt over next 2 years (n=5,474)

Brazilian farmers are leading biologicals adoption, driven by specific pests/disease difficulty to control with traditional chemicals CP (e.g. nematodes)

20%+ of global farmers are adopting / willing to adopt biologicals; Brazil is leading the way, followed by European countries

Sustainability practices adoption and willingness to adopt

% respondents currently adopting or willing to adopt over the next 2 years

Q: What is your level of adoption regarding the following sustainable farming practices?; % respondents currently adopting or willing to adopt over the next 2 years (n=5,474)

Carbon program adherence

Q: Have you participated or plan to participate in carbon programs?; % of respondents (n=5,221)

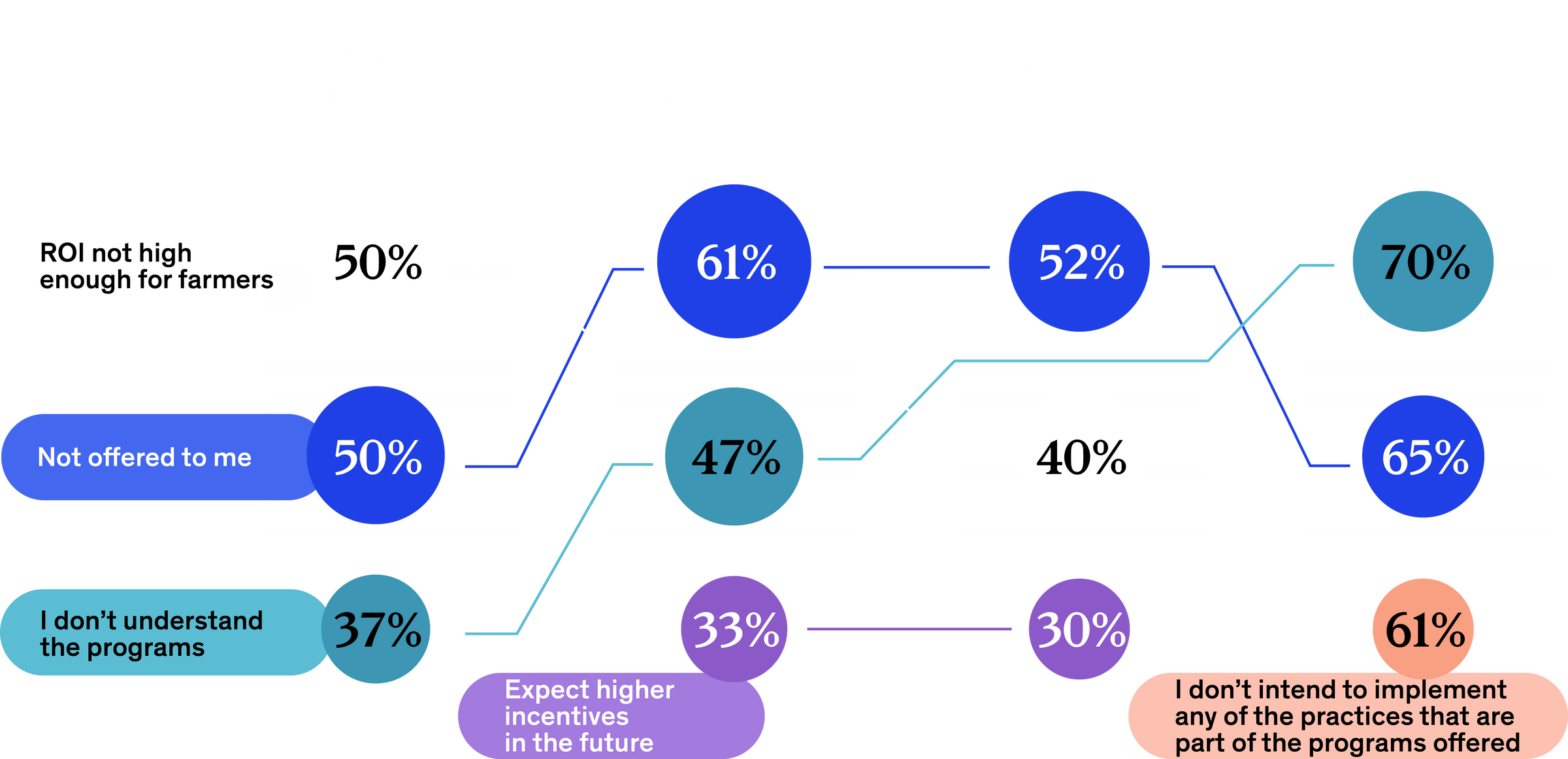

Top 3 challenges to participating in carbon programs

Q: What are the top reasons why you have not yet or will not participate in a carbon program? Rank top 3; % of respondents (n=2,014)

6

considerations for farmer-facing organizations

Consider omni-channel solutions

to engage more and earlier with farmers, enriching personalized offline and online experiences

Become the “innovator” and partner of choice

when farmers are looking to try new products and technologies to drive yield and reduce costs

Offer timely and personalized products and services to farmers

using in-season analyses to target the right customers at the right time and adapt their engagement model

Support farmers during these uncertain times

by helping them capture opportunities (e.g., offer products/services to capitalize on crop prices & yield)

Help farmers monetize the adoption of sustainable practices,

orchestrating the agri value system and finding ways to support implementation and expand penetration and adoption of new practices

Make sustainability programs accessible and simple

Rigor and traceability are key for linking actions to environmental impact and end consumers

Related links

Authors

Nelson Ferreira

Senior Partner

São Paulo

McKinsey & Company

David Fiocco

Partner

Minneapolis

McKinsey & Company

Vasanth Ganesan

Partner

New York

McKinsey & Company

Maria Garcia de la Serrana Lozano

Associate Partner

San Francisco

McKinsey & Company

Ana Luiza Mokodsi

Engagement Manager

São Paulo

McKinsey & Company

Otto Gryschek

Director of Strategy and Operations

Chicago

McKinsey & Company